LIFESTYLE

CIBIL score: Bad CIBIL score becomes the reason for breaking of marriage, how to increase your CIBIL score? Know smart tips..

The groom had entered the wedding, the bride was standing with the garland in her hand and the relatives were busy dancing and singing. But then someone checked the groom's CIBIL score and the marriage broke. This may sound like a film scene, but recently a similar case came to light in Murtijapur, Maharashtra. In such a situation, along with the horoscope, financial stability has also become important for marriage.

In today's time, CIBIL score is not limited to just taking a loan, but along with looking at the relationship and family before marriage, now people have also started looking at the credit score of their future spouse. This news also made it clear that now marriage is not limited to just love and the union of families, but the financial background has also become important.

So let's know why financial compatibility is important. Along with this, we will know what is CIBIL score and how it can be improved.

Why is financial compatibility important before marriage?

Earlier, only family background, relationships, and personal qualities were considered before marriage, but now financial compatibility has also become an important factor. Many people ignore their partner's habits, spending patterns, savings, and investment planning. But tension regarding money can increase after marriage if the financial habits of both do not match. If the partner has a lot of debt and there is no planning for its repayment, then it can increase problems in the future.

On the other hand, if a partner spends, saves, and invests according to his income, then such a partner can prove to be a better life partner after marriage.

Why do Indian couples not discuss money openly?

It is still not common to talk openly about money in relationships in India. According to a survey by YouGov:

32% of Indian millennials and Gen Z had taken a personal loan without telling their partner.

Only 30% of Indians trust their partner completely in matters of money.

68% of Indian women prefer to choose a financially stable partner over a partner with a high income.

But despite this, couples avoid discussing finances, which can later create tension in the relationship.

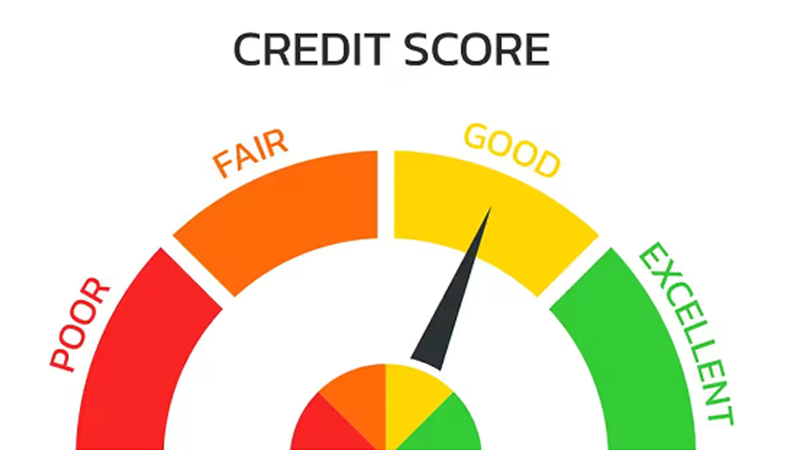

What is the CIBIL Score?

When you go to take a loan from a bank or financial institution, they first check your CIBIL score. Let's know the meaning of the CIBIL score.

It is a 3-digit rating, which ranges between 300 to 900.

A CIBIL score of 750 or more is considered good and it makes it easier to get a loan.

If your CIBIL score is low, then banks hesitate to give loans or give loans at high interest rates.

Reasons for Low CIBIL Score

If your CIBIL score is low, it can affect your financial decisions. Let's know the main reasons for this:

Not paying loan or credit card on time - Delay in EMI or credit card bill drops the score.

Taking too much debt (High Debt Burden) - If the loan is more than your income, then the bank may consider you risky.

Overuse of credit card - If you are spending close to the credit card limit every month, then the score can be bad.

Applying for a loan repeatedly - Applying for a loan repeatedly makes the bank feel that you need more money, due to which the score can fall.

Not having any credit history - If you have never taken a loan or credit card before, then the bank does not know anything about your financial behavior, due to which the score can be low.

What problems can be caused by a poor CIBIL score?

If your credit score is bad, then you may have to face many problems. Like it may be difficult to get a loan. There may be a problem in getting a credit card. At the same time, even if you get a loan, the interest rate will be high.

How to improve CIBIL score? (Improve CIBIL Score)

If your CIBIL score is bad, then there is no need to panic. You can improve it with some smart ways:

1. Pay all loans and bills on time

Never default EMI and credit card bill.

Try to pay the entire credit card bill every month.

2. Avoid taking too much debt

If there are already many loans running, then avoid taking a new loan.

Do not use more than 30% of your credit limit.

3. Do not close the old credit card

Closing the old credit card without reason can affect your credit history.

4. Take a new loan wisely

Avoid applying for a loan repeatedly, because your CIBIL score is checked every time, which can reduce the score.

5. Check your CIBIL report regularly

To see if there are any wrong entries in your report.

If any mistake is found, get it corrected immediately.